Amazon has engulfed nearly every aspect of retail and is positioned for more. Its North American sales have quintupled since 2010. Between 2015 and 2016, Amazon captured well over a third of all American online retail sales—including 43 percent in 2016. Moves to vertically integrate its supply chain by solidifying an ocean freight license, marketing in-home deliver, and creating a $1.5 billion cargo airline would make the 1920s robber barons blush. Traditional retailers looking to compete against Amazon face even bigger obstacles: Amazon’s market capitalization. In the last 10 years, retailer mainstays Sears, JC Penny and Kohls lost an average of 82 percent of their value. Amazon gained 1,934 percent, allowing it access to the cheap capital the finances its growth.

It isn’t just the company’s world-class logistics traditional retailers are facing—it’s the threat Amazon poses to different retail segments combined with its reputation among consumers. The recent Whole Foods acquisition instantly erased $12 billion in shareholder value from six major food retailers. Meanwhile, consumers love Amazon. It is one of the most trusted brands in America. It controls one of the world’s least exclusive clubs: in 2017, 80 million Americans were members of its Prime 2-day shipping and entertainment program (by contrast, France has a population of about 69 million people).

How can retailers compete with Amazon? It’s an 800-pound gorilla that is beloved by consumers, with exceptional operations and a limitless pocketbook.

This is an attempt to scratch the surface of the tactics and strategies that powered history’s Fortune 100 retailers. The analysis is based off a data set created from Fortune Magazine, industry publications, Capital IQ, and public financial documents. It was then organized across 10 industries, 22 supersectors, and 30 sectors through Russell’s Industry Classification Benchmark (ICB). Drawing on this data, six major insights emerged—each powering the eras’ greatest retailers. Some are obvious, some aren’t. All are required if modern retail executives want to compete against Amazon.

1890-1995: A Brief History of American Retail

The bulk of this analysis will focus on retail life post-1995. Why? Three reasons.

- The SEC’s EDGAR (SEC Filings) database starts in 1994.

- Forbes added retailers to the Fortune 500 list in 1995.

- Amazon was founded in July of 1994.

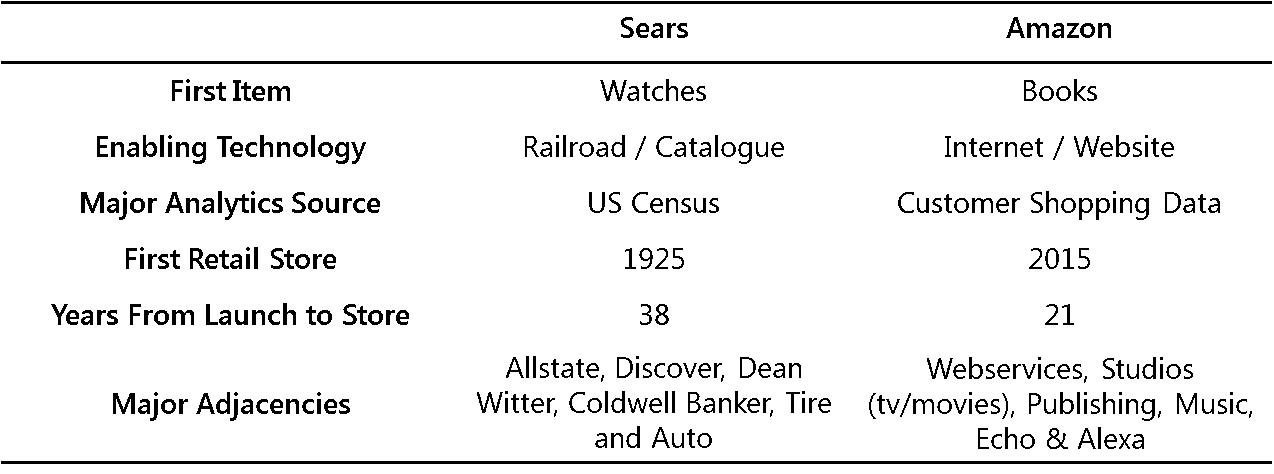

Of course, American retail has a long and lucrative history and there’s no better place to explain its evolution than the Amazon of the 20th century: Sears.

Sears was founded in 1893. Like Amazon 100+ years later, it focused on selling one item—watches. It used the network technology of the era (railroads) to reach customers across America. After initial success, Sears expanded into jewelry, and within a decade, its ubiquitous catalog offered everything a family could need—from houses to blouses–delivered by rail, and backed by a guarantee. As population trends shifted, Sears complimented the mail order operation with downtown department stores. When US macro-trends moved to suburbs, Sears became the de facto anchor of suburban malls. In the middle of last century, Sear’s domestic annual revenue was about 1 percent of U.S. GDP. During this time Sears spun off adjacencies that generated billions of dollars: All State Insurance, Discover (the first rewards card), automotive care, and stock brokerages.

Sears was founded in 1893. Like Amazon 100+ years later, it focused on selling one item—watches. It used the network technology of the era (railroads) to reach customers across America. After initial success, Sears expanded into jewelry, and within a decade, its ubiquitous catalog offered everything a family could need—from houses to blouses–delivered by rail, and backed by a guarantee. As population trends shifted, Sears complimented the mail order operation with downtown department stores. When US macro-trends moved to suburbs, Sears became the de facto anchor of suburban malls. In the middle of last century, Sear’s domestic annual revenue was about 1 percent of U.S. GDP. During this time Sears spun off adjacencies that generated billions of dollars: All State Insurance, Discover (the first rewards card), automotive care, and stock brokerages.Then some have argued, Sears became a victim of its own success. The growth brought in by the successful adjacencies distracted executives from their underlying retail competitive advantage. The millions of dollars earned through the Discover card boosted the bottom line, but the retail operations were stuck in the 1960s. Walmart, Home Depot, and other big-box retailers took advantage.

Insight 1: Process, not technology, can drive massive innovations

Today, cutting-edge technology is often touted as the solution to retail’s biggest problems. Most trend pieces cite Omnichannel and Mobile as key competencies each company must master if they want to compete against Amazon. These are potentially important, but they aren’t the only way to drive value. Instead, think about the underlying business processes the power your business. In the 1920s, Sears shipped products from its factory partners directly to its customers. Think about that for a second. A customer placed an order, Sears forwarded it along, the factory produced it, and the factory shipped it. Millions of orders were processed, all without a single computer or mass-telecommunications coordinating the transactions. The process led to mass disorganization. “For heaven’s sake,” a customer wrote to Sears after receiving five errant orders, “quit sending me sewing machines.”

This changed in 1906 when Sears built a centralized distribution center in Chicago and required manufacturers to ship products there. Once inventoried, Sears assigned every order a shipping room and a shipping time that dictated the process. For simplicity, let’s say that you ordered a dress and boots. Sears would assign the order shipping room (B) and a shipment time (10 am). The dress and boot departments were notified and responsible for getting the items to Room B by 10 am. At 10 am, the order would ship. If a dress arrived at 10:15 am the Dress department had to ship it separately and was billed the cost.

Insight 2: Capture analytics true value by understanding their context

Today, Amazon is often credited with revolutionizing retail with its mass collection and analysis of customer data. It has and it deserves credit, but this isn’t particularly unique. Sears transformed the industry in the 1920s through its analysis of the Census of Population and the Statistical Abstract of the United States. After reading and analyzing the report, Executive Robert Wood projected that the US population would move away from the frontier and back into cities. On its own, this data suggests building department stores in downtown urban centers—like Woolworths. But Wood understood the technological context in which this was operating. Automobiles would make the population more mobile—decreasing the importance of rail transport and downtown department stores. In 1925 Sears opened its first urban department store. By 1929 it had over three hundred, most on the outskirts of cities, where the cheap rent and large size allowed them to double and distribution centers.

Insight 3: Master the era’s product presentation

The Sears catalog was effectively the Amazon.com of its time. It “presented such a cornucopia of goods,” Professors Graff and Temin wrote in their definitive business study of Sears, “that it created what we might now call a virtual reality in the minds of Sear’s rural customers.” With refined copywriting and detailed pictures, Sears mastered the art of 2-D presentation.

As consumers transitioned from catalogs to stores, Retail and CPG executives spent the last five-plus decades perfecting the in-store experience. Shopper marketing, packaging design, and branding were all major components to success. But today the trend is shifting. The rising impact of e-commerce has made the 2-D presentation a vital component to retailer success. While in-person shoppers demand their stores become a place to socialize rather than merely a place for transactions. It isn’t going to be easy, but retailers need to become great at presentation instore and online.

1995-2010: Pre-internet big boxes

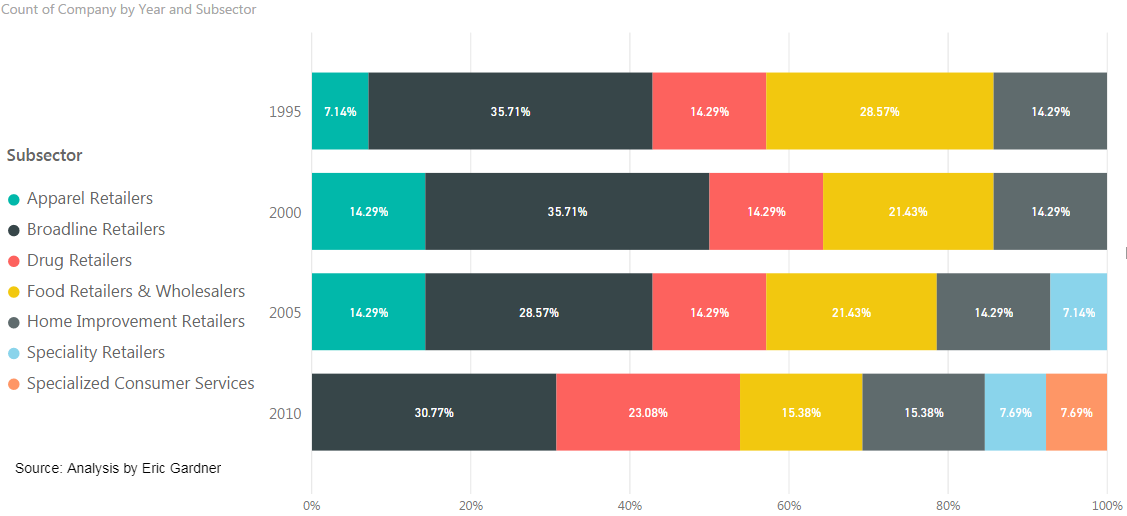

Nineteen retailers reached the Fortune 100 during this 15-year era. They can be loosely categorized into the following:

- Apparel: J.C. Penney and Macy’s

- Broadline: Costco Wholesale, Kmart Holding, Sears, Target, and Walmart

- Drug: CVS/Caremark, Rite Aid, and Walgreens

- Food: Albertson’s, American Stores, Kroger, Safeway, Winn-Dixie

- Home Improvement: Home Depot, Lowe’s

- Specialty: Best Buy

- Specialized Consumer Services: Amazon

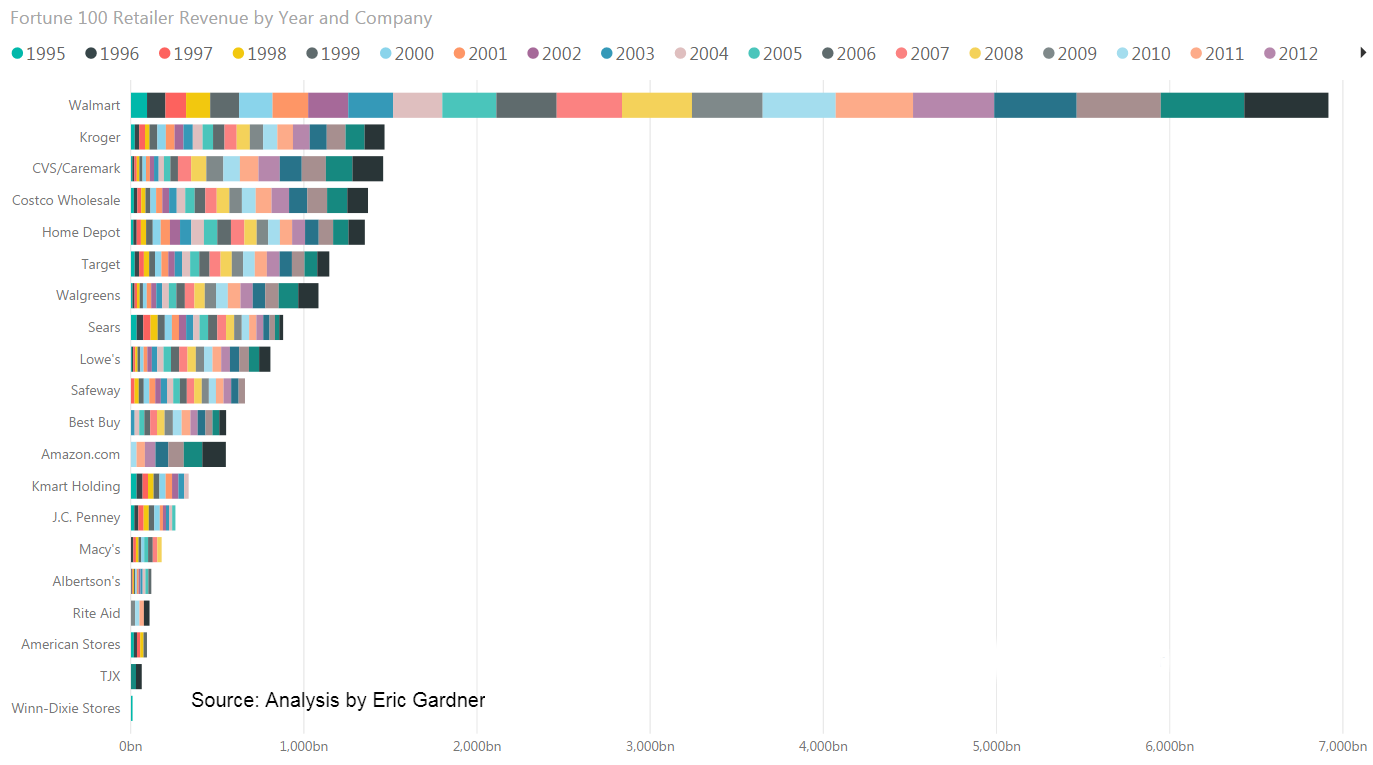

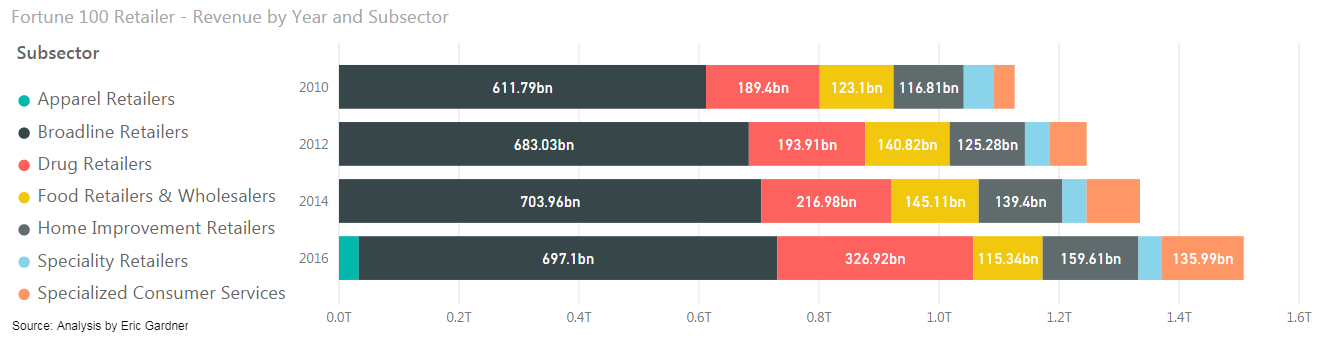

Even though the total number of retailers in the Fortune 100 remained relatively constant (between 13-14) the distribution of revenue did not. In fact, the first thing you notice about the chart below is that Walmart was the clear winner of the 1995-2010 retailer revenue wars. In fact, in that 15-year span it captured more revenue than Home Depot, Kroger, Costco, Target, and Sears combined. In 1995 Walmart had about $95 million in revenues. Its next closest competitor was Sears, who tallied $35 billion dollars. By 2010 Sears earned about $42.6 billion while Walmart neared $422 billion.

Insight 4: Develop a Talent for Cheapness

How did Walmart do it? According to the Atlantic’s Derek Thompson, the company amassed power through a “talent for cheapness”. In the era before Sears built stores on the edge of cities, Walmart built in rural areas. This meant cheaper land, cheaper labor, and cheaper advertising costs. It also used its size to convince vendors to build production near Walmart stores. This meant it could run trucks back to distribution centers 60 percent full. Combined, Walmart adopted the famous “Always Low Prices” strategy.

Insight 5: Master an Integrated Supply Chain

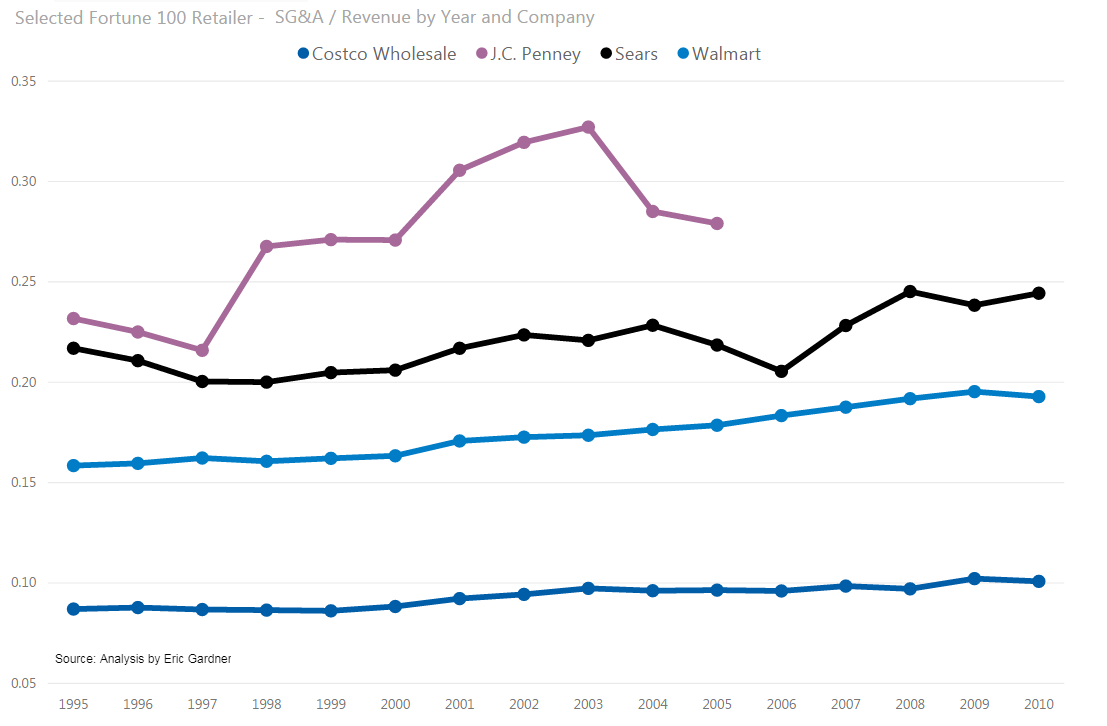

Companies that leverage technology, in practical ways, will find a massive operational advantage. Very early in its ascent, Walmart invested in technology to efficiently manage its shelf space. Instead of periodic counts by humans, Walmart monitored every piece of inventory entering and exiting the store. Workers scanned products in and registers automatically recorded what products sold and compiled what were effectively continuous inventory reports back to management. Managers could then tell, not only what products were selling, but what individual brands were hot, and the impact aisle locations had on sales. The company then used its vast scale to extract discounts from vendors on massive orders on popular items—knowing that it would quickly off-load whatever it purchased. Home Depot began using a similar system in the late 1980s that allowed it to slash prices within home repair. On the other hand, Sears was primarily ordering goods on a store-by-store basis, through individual departments, without the mass of consumption data. The impact of the investment is profound.

2010 – Present: Compete Against Amazon

The most impressive company on this list is the reason for this article: Amazon.

Insight 6: It’s hard to compete against Amazon, because it isn’t a traditional retailer

Ten years ago, Amazon had a market capitalization of about $16 billion—making it the 11th most valuable retailer in America. As of this writing, it is by and away the most valuable–worth nearly $500 billion. The drivers of the growth are numerous. Some are external (rise of the internet, increasing tech aptitude) others are internal (phenomenal operations, bold vision, risk-taking culture). I’ve discussed a few in the intro to the piece, but what I want to talk about here is an undeniable aspect of Amazon that makes it unlike almost any other business in history.

It doesn’t really have much interest in making money in the short term.

In the last five years, Amazon turned a profit three times. In fact, without AWS (its cloud service provider) that number would be zero. CEO Jeff Bezos is upfront about this. In the company’s 2012 annual letter he responded to criticism that the company was “a charitable organization being run by elements of the investment community for the benefits of consumers,” by arguing that he was simply managing the company for the future. “Take a long-term view,” he wrote, “and the interests of customers and shareholders align.” Consider the

- In 2014, Amazon wrote down a $170 million Fire phone, and no one cared

- In 2016, It lost $7.2 billion due to 2-day shipping costs, which is classified as a marketing expense

- In 2017, it more than doubled what HBO spent on content when entertainment is an ancillary business

I don’t point this out to belittle Amazon. I genuinely admire what the company has accomplished. However, retailers and consumer goods companies looking to compete against Amazon must realize they aren’t lining up against a normal company. Shareholders are okay with short-term losses because it has the ability to deliver unbelievable service and craft an amazing story. It isn’t held to the standards of traditional competitors.

What to do next

A look through history shows that retail industry has always been in a constant state of change, but it also has a funny way of repeating itself. Retailers who are gearing themselves up to compete against Amazon face a significant effort, but it doesn’t need to be revolutionary. It requires a rethinking of business processes, context-driven analytics, transformation of merchandising, squeezed out supply chain costs, and integration of the supply chain.

None of these are easy. But looking to the past will strangely help create a retailer that is forward-looking and operationally efficient while enabling it to take advantage of the newest trends.

Note

This originally appeared on my LinkedIn profile.

It doesn’t reflect the views of my employers.

Special thanks to Aaron Chio, Carrie Francis, Caitlin Pardo, Steve Rosenstock, Evan Shirley, and Peter Tzefronis for their feedback on earlier versions of this post.